Lawrence Lepard who supplied this analysis runs a fund, the mission of which is to provide “MONETARY DEBASEMENT INSURANCE.” That’s merely a turn of phrase, but its meaning IN THESE TIMES is clear.

Lepard is:

Pro Blockchain/Bitcoin.

Anti all other crypto.

Wary of all “phantom” collateral.

Convinced we’re experiencing “monetary chaos.”

Likes gold and silver mining stocks.

Blames the Fed for creating an economy where “value” cannot accurately be established.

Blames the Federal government for abetting the Fed in its misguided policies.

Fears a higher cost of capital will create a NEGATIVE FEEDBACK DOOM LOOP.

Believes the Fed will inflate away debt rather than have the US RISK DEFAULT.

Convinced that the current “deflationary impulse” will REVERSE as soon as something serious breaks in the markets.

AS FOR ME, I’M BIG ON CASH. AND SINCE INFLATION HURTS A SOLID CASH POSITION WHILE HIGHER INTEREST RATES IN A DEFLATIONARY ENVIRONMENT ENHANCES ONE, I’M STRICTLY FOR DEFLATION EVEN IF IT CAUSES A DEPRESSION AS NOT EVERYONE EXPERIENCES A DEPRESSION THE SAME.

ESPECIALLY THOSE WHO ARE GETTING 5% ON SOLID CASH BALANCES. SO, IF THE FED NEVER PIVOTS, THAT’S ENTIRELY OKAY WITH ME.

Or, to paraphrase James Carville, IT’S ENERGY, STUPID!

From Gail Tverberg:

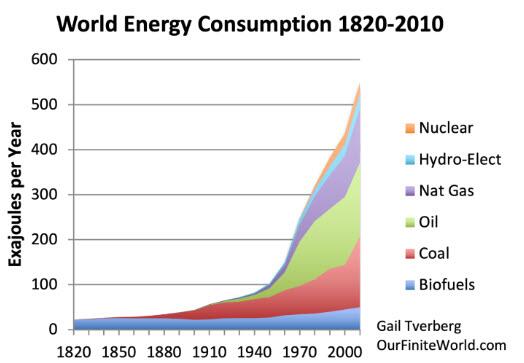

“Most people do not understand that the world economy is a physics-based system, powered by energy. If the energy is suddenly much less available, there will be a huge problem. The world economy has been powered by a rapidly growing supply of energy for over 200 years.”

AND COUNTING. MAYBE.

Note how closely the above chart tracks the course of MODERNITY and the GREATER PROSPERITY that accompanied it. That’s no COINCIDENCE. Without hydrocarbons, the 1860 to 2000 SPIKE IN LIVING STANDARDS would not have happened.

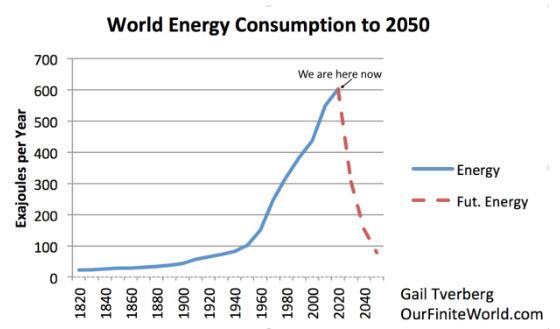

But that was the GOOD NEWS. Check out the chart below:

Says Tverberg:

“Everything I can see says that world leaders are not able to face the possibility that the world is already running seriously short of oil and coal. Future supplies are likely to be much lower, and much more expensive, if they are available at all. Other energy types (including natural gas, nuclear, hydroelectric, wind and solar) are simply add-ons to a system built using coal and oil.”

SO MUCH FOR A SELF-SUSTAINING CORE GREEN ECONOMY, something I’ve SERIOUSLY DOUBTED WAS FEASIBLE since around 2006. And where, I ask, is the EVIDENCE to CONTRADICT ME?

Tverberg continues:

“The amount of energy the economy requires depends very much on population. The greater the world population, the more oil is needed for food production and transportation. Non-oil energy is a bit more flexible in quantity than oil, but the total quantity of energy per capita needs to keep rising to prevent very adverse outcomes.”

Note that the RAPID ENERGY GROWTH PERIOD between 1950 and 1980 has long DISAPPEARED in the REARVIEW MIRROR.

Tverberg:

“Recently published data through 2021 indicates that energy consumption growth is not keeping up with population growth, similar to the situation of the 1930s. This says that the economy is doing poorly. Supply lines are broken; most jobs don’t pay well; many goods that normally would be available aren’t available.“

Note that 2018 was the year in which ENERGY CONSUMPTION peaked. The same was true of the number of automobiles sold that year.

Tverberg turning to the ECONOMIC IMPLICATIONS of all of this:

“We can look back and see how rising interest rates were used to slow the world economy in the 2004 to 2006 period, and how different the economic situation was then compared to now. Even with the rapid growth the economy was making at the time of the interest rates increases, the result was still a deep recession in 2008-2009.”

And don’t WE ALL REMEMBER IT. The OBSCENE GOOSING of the housing market.

Two things stand out about this period:

Tverberg:

“The world economy (as shown by rising energy supply) was growing much more rapidly during the 2001 to 2007 period than it is in 2022. All the world economy is trying to do now is get back to where it was before the 2020 shutdowns, in terms of energy consumption per capita.

“Eventually, there was a bad reaction to the higher interest rates of 2004 to 2006, but this did not come until 2008-2009. This was a much longer lag than most people would expect.”

“Now, in 2022, we cannot get energy consumption per capita up to the 2018 and 2019 levels. There are many unfinished automobiles, waiting for missing parts . . . Broken supply lines leave many store shelves empty. It is not that DEMAND is unusually high; it is the SUPPLY of the energy products we need to grow food and to transport many finished goods that is not available.” (my caps)

“If the problem is an inadequate supply of finished goods and services (due to broken supply lines and low wages for workers), then raising interest rates is ENTIRELY THE WRONG MEDICINE. It will cause even fewer automobiles and appliances to be made. It will cause many current workers to be laid off. Such an approach, when the world is trying to deal with too few workers, will tend to make the situation worse, rather than better.” (my caps)

Except that RAISING INTEREST RATES is the ONLY WAY to BEAT BACK inflation.

WHAT FRESH HELL (DILEMMA) IS THIS?

Tverberg:

“The trend in fossil fuel supplies is concerning. Both oil and coal are past peak, on a per capita basis. World coal supply has been lagging population growth since at least 2011. While natural gas production is rising, the price tends to be high and the cost of transport is very high.”

Tverberg concludes:

“Governments and academic institutions have gone out of their way to avoid telling the world how important energy of the right types and in the right quantities is to the economy.”

“Once the economy starts heading downward, it is not clear that the economy can ever “catch itself” and start back on an upward path again, even for a short while.”

For example, check out this chart of WEEKLY US FIELD PRODUCTION OF CRUDE OIL:

The hiccups are APPARENT.

Tverberg’s closing, sobering words:

“With less energy supply available, the whole world economy that we know today seems likely to start falling apart. Fewer goods will be available through international trade. It is cheap energy that has allowed today’s economy to function. Once this cheap energy is depleted, the world economy will need to shrink back in many ways, at once.

“We don’t really know precisely what lies ahead, and perhaps, this lack of knowledge is for the best. We cannot even imagine a world economy changing rapidly for the worse.”

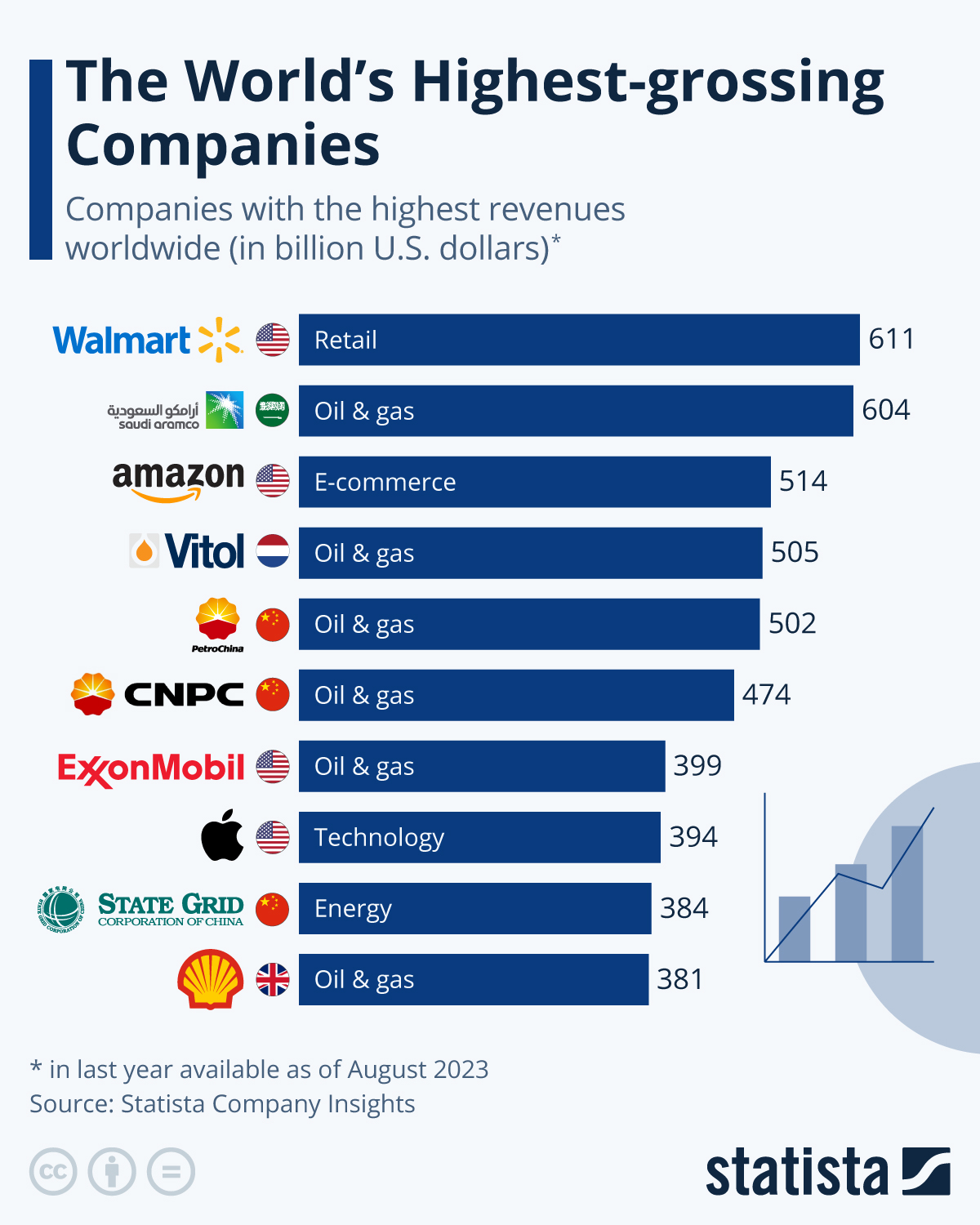

What it shows is that the heart-and-soul sectors of the GLOBAL ECONOMY are RETAIL, ENERGY, TECH and HEALTHCARE.

But a deeper dive SHOWS MORE.

And in order to reveal that additional information, I’ve grouped these companies in a way that varies somewhat as per their SECTORS as listed in the graphic.

First, I see AMAZON as more retail than e-commercial but CVS, since it owns Aetna Insurance and sells prescription drugs and OTC medications, as more a healthcare company than a retailer.

With that in mind . . .

The combined revenues for WALMART, the other retailer listed, and AMAZON total $1.043 trillion, whereas the revenues for CVS plus the other healthcare company listed in the graphic, UNITED HEALTH CARE, total $569 billion.

The next group shown are all energy companies, one listed as such — STATE GRID CORPORATION OF CHINA — and the other three, oil & gas companies: SAUDI ARAMCO, CNPC and SHELL. Their combined net revenues total $1.307 trillion.

If as a COMPLEMENTARY BUSINESS, carmaker VOLKSWAGEN’S revenues are lumped together with those of the energy producers, the combined revenues total $1.592 trillion.

If, instead, VOLKSWAGEN is viewed more as tech company and its revenues combined with APPLE, the sole PURELY TECH company listed, the resulting total is $651 billion.

What emerges then is a clear picture of how the current global economy — at least as per its ten leading companies as measured by sales — is, SECTOR-WISE, weighted.

Out of the $3.570 trillion in total revenues produced by these companies, the breakout by SECTOR — ON A PERCENTAGE BASIS — is as follows:

Energy = 36.61%

Auto = 07.98%

Energy + Auto = 44.59%

Retail = 29.22%

Healthcare =15.94%

Tech = 10.25%

Tech + Auto = 18.24%

Of interest TO ME is that almost HALF OF THE GLOBAL ECONOMY is dedicated to the production of a) energy products and b) the land-based vehicles which CONSUME much of that energy.

In other words, CARS are KEY TO HOW WE LIVE.

Yet, MUCH OF THE ENERGY WE USE AND WILL CONTINUE TO NEED IN ORDER TO MAINTAIN AN AUTOMOBILE BASED SOCIETY IS ALMOST UNIVERSALLY TAKEN FOR GRANTED.

At the same time, the ENERGY SECTOR — both combined and in combination with the AUTO SECTOR — STILL DWARF THE TECH SECTOR where all of the SO-CALLED ACTION is taking place. And that’s true even when TECH and AUTO are combined.

So, if the ENERGY SECTOR of the economy breaks down, not only does it become virtually impossible to run our world in a way where we can REASONABLY EXPECT TO SURVIVE, but it also WIPES OUT AT LEAST HALF OF OUR WEALTH.

And if you factor in that about 80% of everything we currently use is a HYDROCARBON BYPRODUCT, an ENERGY COLLAPSE cannot help but cascade EXTREMELY QUICKLY into GAME, SET and MATCH for HUMANITY.

Maybe this is MORE INFORMATION THAN YOU NEEDED. Still, there it all is for those WHO WISH TO USE IT.

The BAILOUTS — and flat-out NATIONALIZATIONS — are ONLY BEGINNING.

Here, we’re talking UNIPER, Germany’s DISTRESSED NATURAL GAS UTILITY.

One number to consider. Uniper probably is paying currently ~€30 million extra for the gas it's buying in the spot market. Multiply that for 365 days: ~€11 billion. And that's one single European utility. Now think about other big buyers of Russian gas. And start multiplying. https://t.co/6hKzinI7Pw

“While flows through the Nord Stream 1 pipeline resumed Thursday after 10-day maintenance, deliveries remain down around 40% capacity, and injections into storage for winter were around 65% full.”

More ZH:

“Uniper shares surged as much as 7% after Bloomberg reported the deal was in the final stage earlier this morning but have since reversed and are down 16%. Shares of the utility have plunged more than 78% this year, valuing the company at 3.2 billion euros.”

War with Russia, no matter how well-intentioned, DOESN’T COME CHEAP.

With a group of former JP Morgan precious metals traders currently on criminal trial in front of a federal jury in Chicago, accused of engaging in a racketeering conspiracy involving precious metals price manipulation, commodities fraud and trade spoofing, while another group of their colleagues have already pleaded guilty,now is a good time to ask how the bank JP Morgan is still considered fit and proper to not only continue to trade in the precious metals markets, but to continue to literally dominate the entire precious metals industry in London, Singapore and New York, with the support of the London Bullion Market Association (LBMA), the Singapore Bullion Market Association (SBMA) and the CME Group (operator of the COMEX and NYMEX).

And, yet, JPM KNOWS ONLY TOO WELL the INHERENT VALUE of PM’s.

Who WILL FILL these vacant offices, and what EXACTLY will they be doing?

We’re STRUCTURALLY SUITED to about a 40 to 50% SMALLER ECONOMY. So, if a SEVERE DEPRESSION on average HALVED incomes, much of not only the LARGESSE we enjoy but also the SURPLUS we take for granted would DISAPPEAR.

“PHILADELPHIA – A team led by researchers at the Perelman School of Medicine at the University of Pennsylvania has used advanced techniques to show that, in a key memory region of the brain called the hippocampus, immature, plastic neurons are present in significant numbers throughout the human lifespan. The findings, published this month in Nature, hope to resolve a long-running controversy over the existence of “adult neurogenesis”—the production of new immature neurons in the mature human brain. The discovery also paves the way for the deeper study of adult neurogenesis and its roles in memory, mood, behavior, and brain disorders.”

Virtue-signaling COMES FULL CIRCLE as the hypocrisy it is.

From Bloomberg ESG analyst, Tim Quinson:

“European-based ESG equity funds have been increasing their investments in energy companies, including Shell Plc, Repsol SA, Aker BP ASA and Neste Oyj, according to analysts at Bank of America Corp. About 6% of the funds invested in Shell this year, compared with none in 2021.”