Looks like that TRIED AND TRUE FORMULA of starting a non-profit around a SEXY CAUSE, getting well-heeled LIBERALS — even at the corporate level — to kick in huge chunks of cash, and then paying yourself handsomely for your own SCHEMING INITIATIVE.

And, yes, THIS HAPPENS.

I have an MS in Urban Policy with a concentration in non-profit FINANCIAL MANAGEMENT, so I know just how this CAN and DOES work.

Ideals? No. It always comes down to POWER AND MONEY.

Denmark said it would lift almost all Covid-19 restrictions and stop designating it a “societally critical” disease on Wednesday in the latest sign that western European countries are easing or even eradicating strict measures brought in to combat the Omicron coronavirus variant.

Magnus Heunicke, Denmark’s health minister, wrote to parliament on Wednesday saying that he would remove all Covid-19 restrictions on February 1, except for testing on arrival from abroad. Just as the Danish government did in September, when it lifted all restrictions, it will also stop calling Covid-19 a “societally critical disease”, meaning that it will no longer have the legal basis to introduce wide-ranging curbs.

“Tonight we can begin to lower our shoulders and find our smiles again,” said Mette Frederiksen, Danish prime minister, on Wednesday evening. “The pandemic is still here, but with what we know now, we can dare to believe we are through the critical phase.”

Denmark is the latest European country in recent days to announce it is dropping most or nearly all measures as it follows in the footsteps of the UK, Ireland and the Netherlands…

This information is taken from the second and final piece on this subject by The Gold Observer’s Jan Nieuwenhuijs.

Here’s my precis/synopsis:

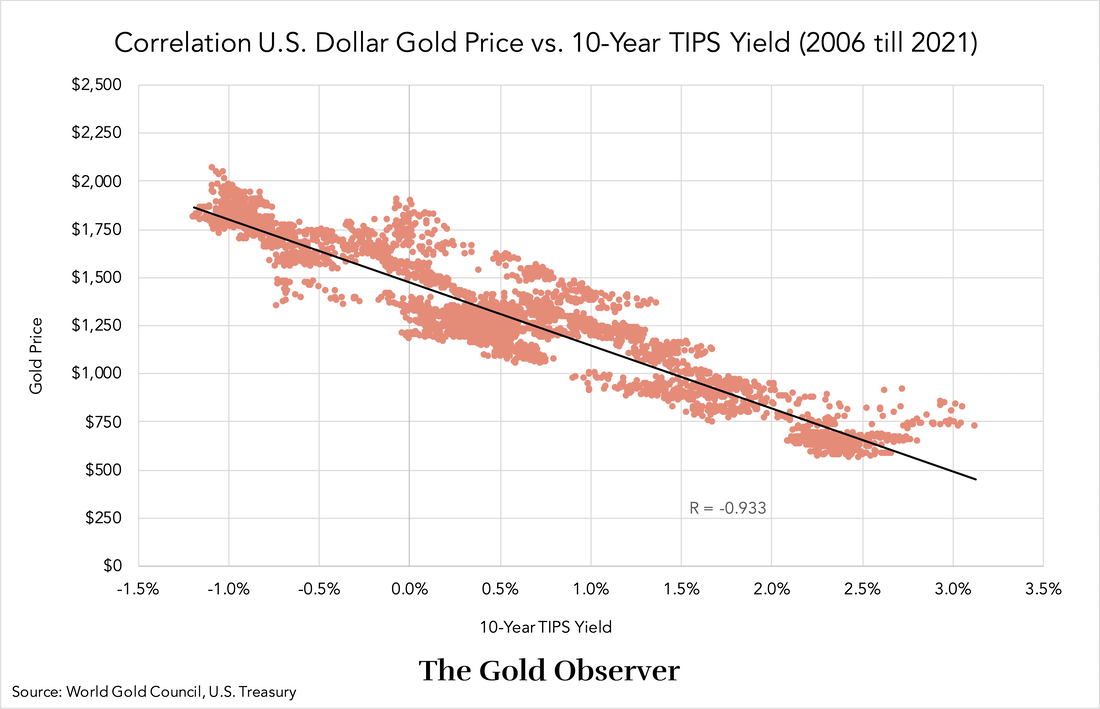

“In the current framework gold is priced based on the 10-year TIPS yield. In my view, the current framework becomes more nonsensical the longer the TIPS yield stays below zero. At the time of writing the TIPS yield is –0.74%.“

Since “2006 the gold price is inversely correlated to ex-ante real interest rates (the expected real rate measured by the 10-year TIPS yield).”

“Causality between gold and the TIPS yield is hard to prove, butthe correlation is very strong (correlation coefficient -0.933) and there is a “rational” narrative.“

“The TIPS yield is the expected real interest rate. The TIPS rate formula is: Expected real interest rate = Treasury rate – inflation expectations. Put differently: TIPS rate = Treasury rate – breakeven rate.”

“A declining TIPS yield drives gold up; a rising TIPS yield drives gold down. The Treasury rate and inflation expectations play a role in the market’s decision to buy or sell gold.”

“Risk free interest rate = real interest rate + inflation expectations. Put differently: Treasury rate = real interest rate + inflation expectations.”

“Because TIPS bonds are compensated for inflation, the market will buy these securities, driving down their yields relative to nominal Treasury yields, until it’s indifferent between holding one or the other. That’s why the difference between the TIPS rate and the nominal Treasury rate is called the ‘breakeven rate.’”

“Consequently, the breakeven rate reflects market-based inflation expectations. If the market expects annual inflation to average 1% over the next 10 years and the 10-year nominal Treasury rate is 3%, the 10-year TIPS yield will be priced at 2% (3% – 1%).”

“The main reason to hold TIPS bonds is because they outperform nominal Treasuries during unexpected increases in inflation. TIPS bonds are a hedge. Needless to say, nominal Treasuries outperform when inflation turns out lower than expected.”

If the TIPS yield is negative — as it is now — “the buyer pays roughly 110% of the principal up front and is returned 100% in ten years’ time without coupon payments. During the lifetime of the bond 100% of the principal is adjusted for inflation, but at maturity the investor has lost -1% per year in real terms.”

“It’s likely that the 10-year TIPS yield stays negative because the total debt to GDP ratio in the U.S. is at a record 370% (public debt to GDP is 120%).The U.S. government can’t allow nominal rates to go much higher in this environment.”

“Meanwhile, printing money and supply chain issues have unleashed inflation. The U.S. government can’t allow nominal rates to go much higher in this environment. Meanwhile, printing money and supply chain issues have unleashed inflation.”

“I think that the longer the TIPS yield stays negative, the more likely gold will decouple and trend higher.”

And once other asset-class bubbles pop, gold will be basically WHAT’S LEFT.

Time will tell if Mr. Nieuwenhuijs’s DECOUPLING THESIS proves out.

This TIMELY data comes from a piece by Jan Nieuwenhuijs of the Gold Observer. It focuses SPECIFICALLY on HOW GOLD IS PRICED. Nieuwenhuijs’s thesis ISN’T BASED on CAUSATION per se but rather on what he sees as extremely strong correlation.

Here’s my precis/synopsis of the piece’s most relevant parts:

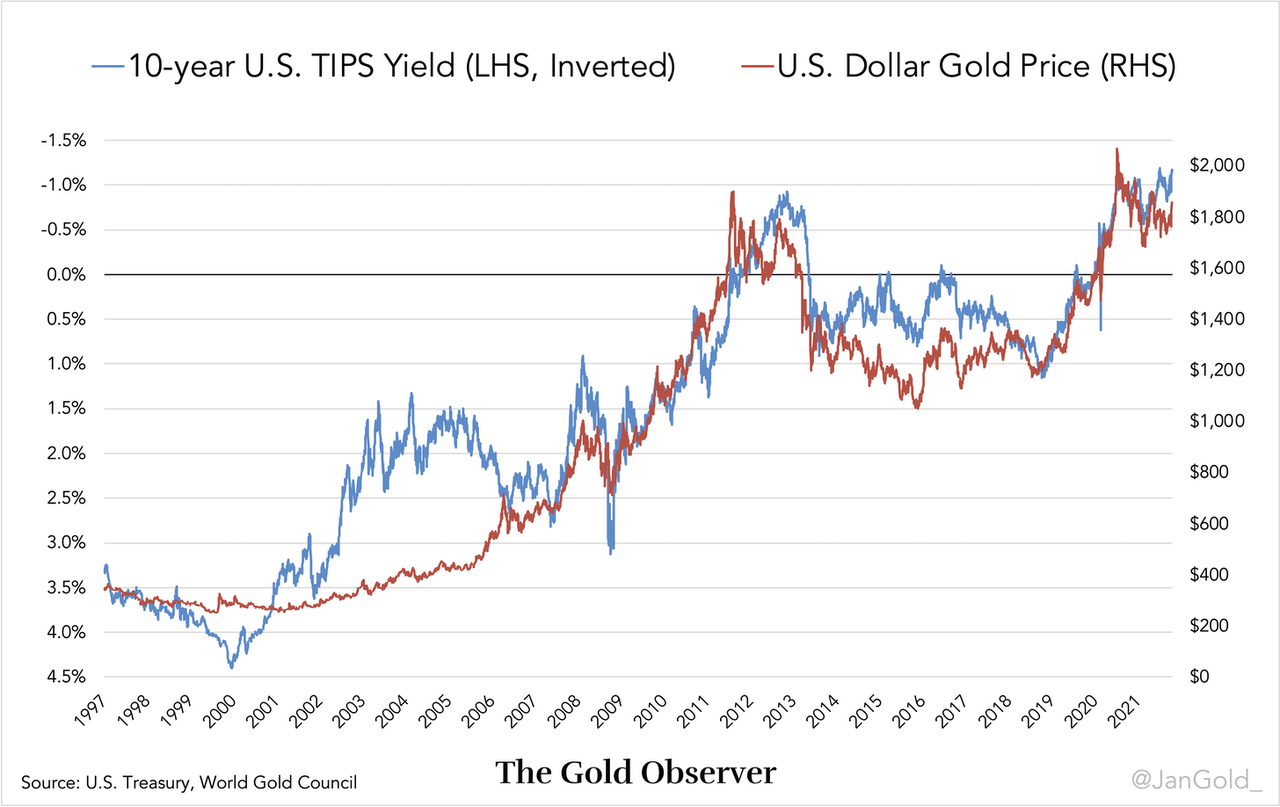

“In general, the gold price in U.S. dollars is set by long-term inflation expectations and interest rates in the United States. The price of gold in other currencies depends on the exchange rate between a particular currency and the dollar.”

These expectations affect — and are expressed via — gold’s “institutional supply and demand.“

“Since 2006 the price of gold in U.S. dollars is inversely correlated to . . . real interest rates derived from the 10-year U.S. Treasury Inflation Protected Security (TIPS). . . .”

As the chart indicates, when the TIPS rate falls, the gold price rises and vice-versa.

When “the real interest rate on government bonds falls, it becomes more attractive to own gold, because gold is the only international reserve asset without counterparty risk. When the real interest rate rises, it becomes less attractive to own gold, because gold doesn’t yield (if not lent out).”

“Because a correction is added when interest and the principal are paid, the market sets the TIPS yield lower than the yield on regular U.S. government bonds (nominal Treasuries). Basically, the market keeps buying TIPS bonds, driving down its yield, until the market is indifferent between holding TIPS bonds or nominal Treasuries, based on what they expect average inflation to be over the next 10 years.”

“The difference between the 10-year TIPS rate and 10-year nominal Treasury rate is thus what the market expects average inflation to be in the next 10 years. This market-based inflation expectation is also called the breakeven rate.”

“In conclusion: “TIPS rate = Treasury rate – breakeven rate. Or, in other words: Expected real interest rate = Treasury rate – inflation expectations.“

Again, this is not a formulation based on strict CAUSATION but rather on what the author sees as extremely strong CORRELATION.

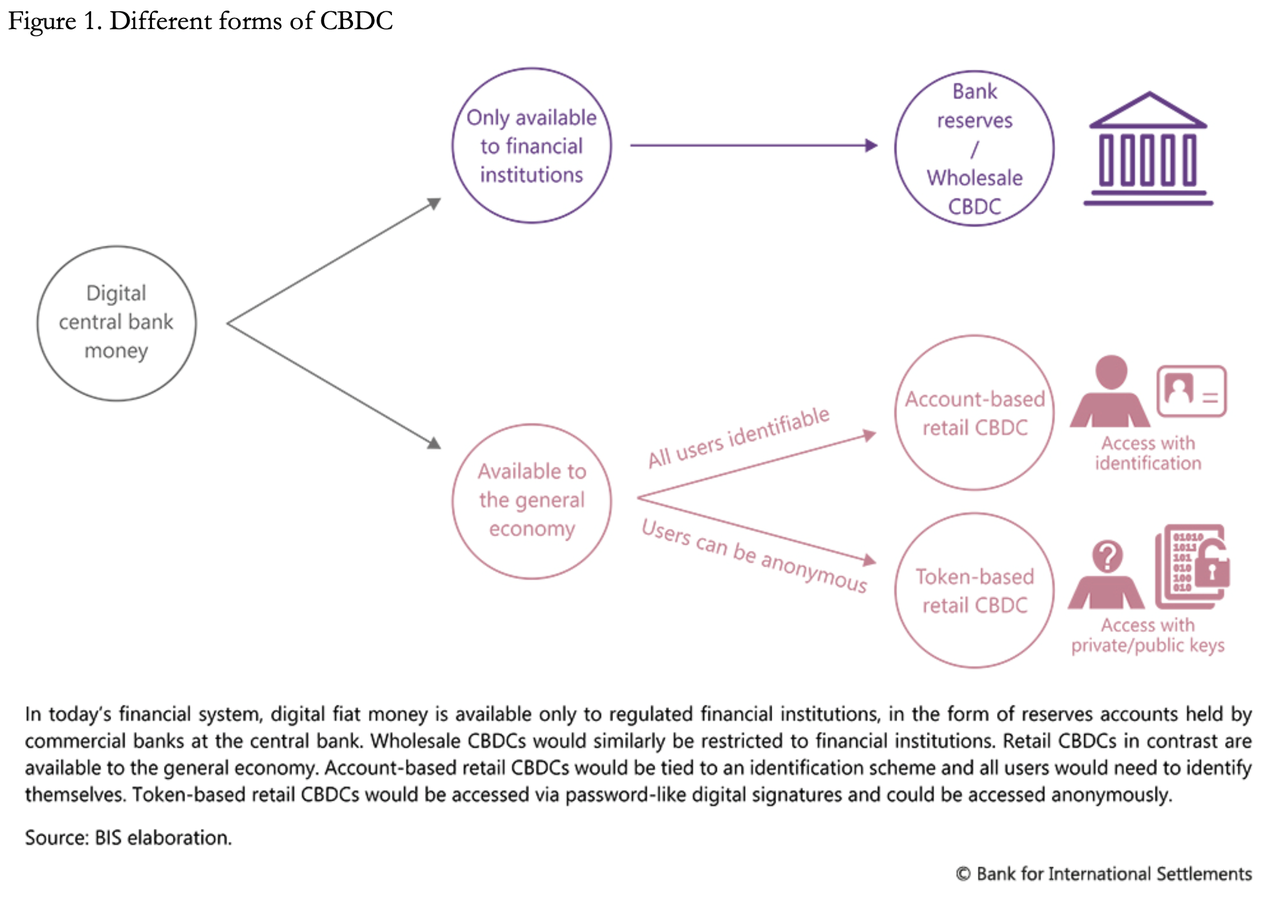

“The CBDC proposition is being sold to us by the central banks as keeping up with the times and taking advantage of the opportunities presented by new technologies to evolve payment systems.“

“There are . . . two separate CBDC functions to consider. There is retail, whereby individuals have direct access to their central bank as counterparty, and a wholesale function for financial intermediaries for international settlement.”

“Whether CBDCs will come into existence is doubtful. To have credibility, their introduction will have to be coordinated at G20 level, and they are unlikely to be widely issued before the end of the decade. That will probably be too late to save the world from a developing financial and monetary crisis which threatens to change everything.”

“Furthermore, the Americans will need to be convinced that their dollar hegemony will not be compromised. And what will almost certainly stop it is the powerful US banking lobby, likely to remind politicians presented with the necessary legislation, that a political survivor is one who once bought, stays bought.”

“But instead of a full-frontal attack on distributed ledgers and the threat they mount to their fiat currencies, major governments everywhere appear to be deploying a strategy of gradual strangulation, hoping the crypto phenomenon will subside. After all, currency isthe preserve of the state and other than mavericks like El Salvador, who wants a private sector alternative?”

“There is one thing that governments and central banks cannot abide, and that is private sector rivals to their currency monopolies.”

This couldn’t be clearer. After all, currency control — via issuance and regulation — is one of the PILLARS OF SOVEREIGNTY. If a nation can’t exert control over its economic output and distribution through control of its financial system, which starts with the currency, how can it be said to have a NATIONAL ECONOMY?

And if not, who then runs the show? 300 million anonymous crypto users guided by the INVISIBLE HAND OF THE MARKET? In what UTOPIA might THAT take place? LIBERTARIAN DISNEYLAND?

Still, monetary scholar that he is, MacLeod then goes on to define a CBDC and how in practice it would work:

“A CBDC is a digital form of central bank money that is different from balances in traditional reserve or settlement accounts. It is a digital payment instrument, denominated in the national unit of account and is a direct liability of the central bank.”

“Two separate functions have been identified. There is a general purpose, or retail function, whereby a CBDC is an alternative to currency cash and commercial bank deposit money. And there is a wholesale function for use between financial intermediaries, incorporating cross-border settlements. Figure 1 illustrates the flows of these two different functions.”

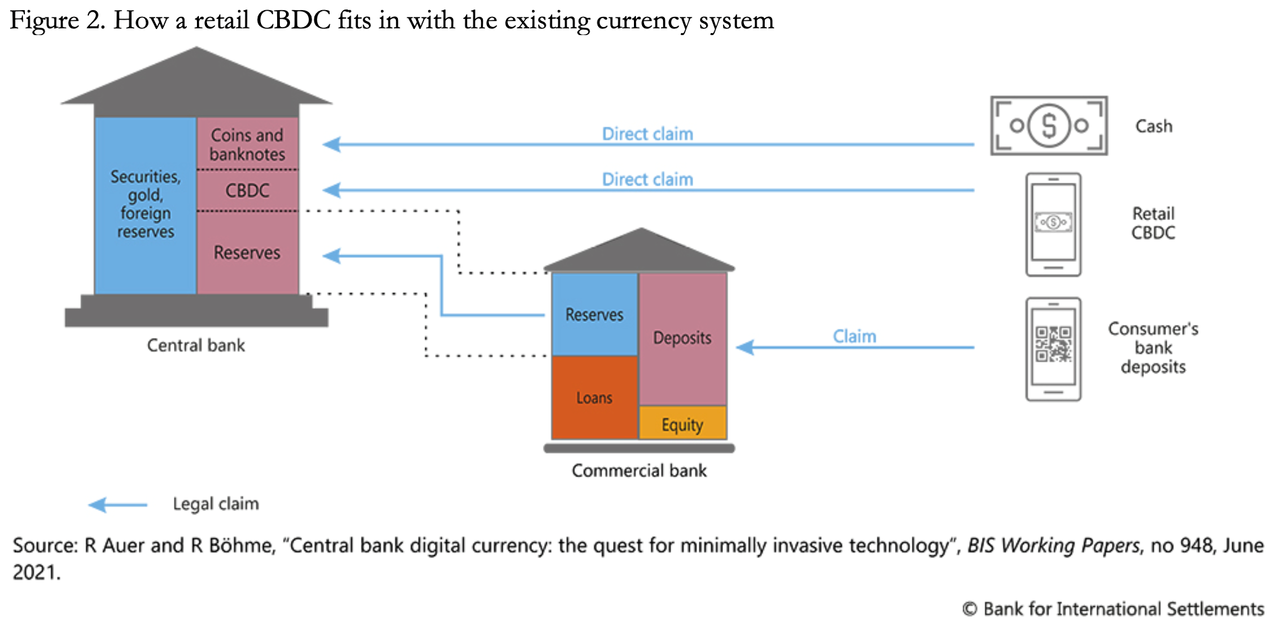

“The adoption of a CBDC requires a central bank to upgrade their banking systems to deal with tens or even hundreds of millions of depositors and businesses — a task whose sheer scale and technological challenges should not be underestimated. Figure 2 illustrates the relationship between a retail CBDC and existing currency liabilities.”

If you wish to learn more about CBDCs, here’s the entire (lengthy) piece:

MacLeod concludes that even should CBDCs be adopted, they will merely “represent an additional source of inflationary finance.”

“Instead of providing solutions for failing economic and monetary policies, CBDCs are a continuing move in the same direction. Nowhere in all the literature emanating from the BIS, or in the Fed’s consultation paper, is there any suggestion that an expansion of the quantity of CBDCs will be offset by a contraction in central bank balance sheets or in the quantity of bank credit. The only offset is the declining use of banknotes and coins, which is a minor portion of the circulating currency.”

As for Bitcoin, MacLeod sees it as just a modified form of FIAT, “and as fiat dies we can expect Bitcoin and its imitators to do so as well.”

STRONG WORDS. Still, there’s much in this piece that makes perfect sense. And for anyone interested in learning the subject, it’s an excellent place to start.

From the Foundation Against Intolerance and Racism (Bari Weiss, Glenn Loury, John McWhorter, Steven Pinker et al):

“On January 20, 2022, FAIR filed a federal lawsuit to stop New York City from enforcing its unconstitutional order prioritizing Covid-19 treatments based on racial categorization and ethnicity.”

This order is worse than NYC’s recently enacted law allowing NON-CITIZENS to vote in MUNICIPAL ELECTIONS.

If you’re Putin or even the AVERAGE RUSSIAN, Croatia’s President, Zoran Milanovic, makes perfect sense.

And, yes, Croatia, is part of NATO. But then, it asks — HOW FAR EAST SHOULD THE ALLIANCE GO? Is Ukraine in the West’s sphere? Or Russia’s? What does HISTORY say?

I’m agnostic on the subject, but I do find it IRONIC that this is CROATIA pleading Russia’s case and not SERBIA.

Russians and Serbs have historically been BLOOD BROTHERS. And while their “kinship” helped trigger WWI, CROATIANS became FASCISTS and marched with the Wehrmacht into Russia on June 22, 1941.